Welcome to Altitude, the bi-monthly drop from Cirrus Capital Partners. We write for founders and finance pros building at the highest level. Expect sharp insights, market movers, and operator-grade tips.

There’s a growing disconnect in venture markets that nobody wants to name:

Too many startups are celebrating ARR milestones that don't mean anything.

$1M. $10M. $100M.

The numbers are loud, but the efficiency behind them is often murky—or worse, manufactured.

Over the past decade, as capital flooded into private markets, the game became one of acceleration.

Raise more → burn more → grow quicker.

Founders were rewarded not for how intelligently they scaled, but for how quickly they could light money on fire and still show up with a hockey stick.

This made sense in a zero-interest rate world. When the cost of capital was close to zero, there was no penalty for spending wastefully. It was all about optionality. Get to the next round, tell a better story, let someone else underwrite the risk.

But that world is gone. What we’re left with is a system that still fetishizes speed, even as capital has become expensive again. Even as the exit window remains jammed. Even as LPs quietly pull back from emerging managers and fund vintages they once championed.

There’s a new reality forming—and many haven’t adjusted.

Capital efficiency is the new alpha

Neil Tewari recently posted a stat that should be burned into every operator’s brain:

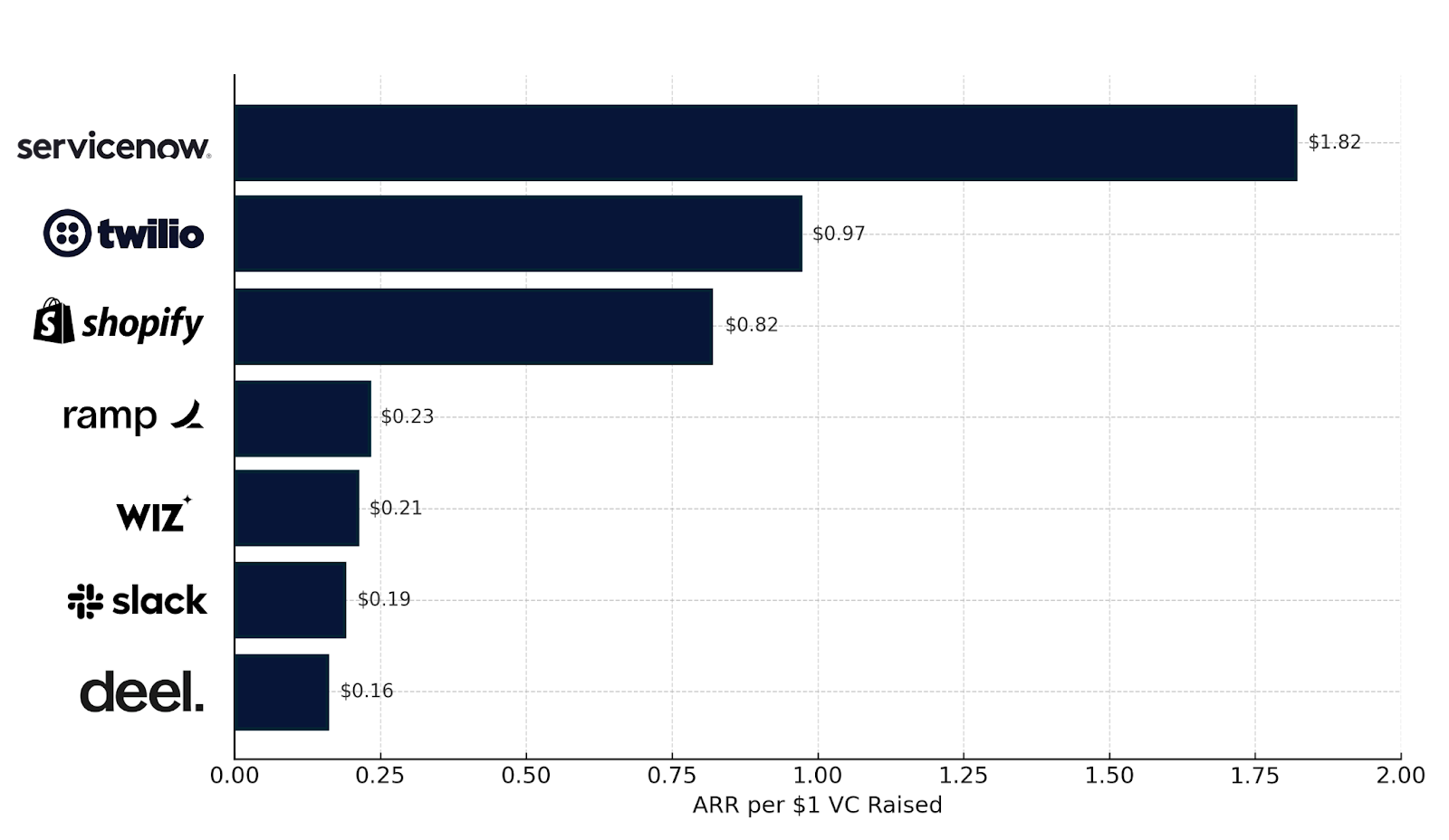

At $100M ARR, these were the dollars raised per $1 of ARR:

ServiceNow: $1.82

Twilio: $0.97

Shopify: $0.82

Ramp: $0.23

Wiz: $0.21

Slack: $0.19

Deel: $0.16

Ignore the absolute ARR. Look at what it cost to get there.

Slack and Deel raised half a billion to get to $100M. ServiceNow? Just north of $180M.

And here’s the punchline: ServiceNow IPO’d in 2012. Slack IPO’d in 2019. Deel hasn’t even exited.

We’ve spent a decade funding speed over durability.

But durability is what defines value.

💡 Founder Tip: If your ARR isn’t paired with margin discipline and repeatable distribution, it’s just noise with a runway. Efficiency isn’t a constraint—it’s a forcing function for clarity.

As rates normalize, capital efficiency isn’t just a nice-to-have. It’s the difference between a business that prints cash and one that never makes it past its next round. Investors know this. LPs know this. And whether founders admit it or not—they know it too.

Neil’s post captured what most founders are feeling but few are saying out loud: fast ARR doesn’t mean it’s real.

The Fed is no longer your friend

Chamath’s 2024 annual letter broke down what may be the most underappreciated macro trend in tech:

The Federal Reserve is losing its grip.

Historically, when the Fed cut rates, long-term yields would fall. Borrowing would get cheaper. Risk assets would rally. Venture would flow. Rinse and repeat.

But in late 2024, that relationship broke. The Fed cut rates three times. And yet—10-year yields stayed high. Why?

Because nobody’s buying what the government is selling anymore. Literally.

Foreign buyers pulled back. Treasury auctions softened. The Fed is quietly unwinding its balance sheet. And with a flood of new debt hitting the market, yields are staying stubbornly elevated. Which means the cost of capital—for everyone—is staying high.

Translation: startups can no longer rely on macro tailwinds to goose valuations or raise their next round.

We are now in a fundamentals-only regime.

Reflexivity at the top of the stack

The effects are cascading down.

Late-stage startups can’t exit because IPOs are stalled. Many are too big to raise another private round, but too fragile to go public. So they turn to internal financing, secondaries, or private credit.

This delays liquidity for early investors. Which shrinks distributions. Which reduces re-ups into new funds. Which tightens the capital available for Seed and Series A.

This is reflexivity in private markets—where weakness at the top tier starves the bottom. Early-stage companies are still promising, but LPs haven’t seen liquidity in years, and the capital spigot has tightened upstream.

This is the part of the cycle where patience dies and discipline decides.

AI as a trapdoor

There’s one exception: AI.

In 2024, over $150B flowed into AI—more than into every other venture category combined.

But here’s what nobody’s really saying: Outside of infra and foundation models, almost none of it is working.

We have a solid wave of copilots, dashboards, and wrappers chasing adoption and churning users. But no killer apps or big time monetization. No legit enterprise-grade stability.

Even the best-funded AI products haven’t escaped the novelty zone. The real traction is in inferencing, chips, and infra—where capital is flowing into hard tech and capex, not SaaS tools with LLMs duct-taped to the front.

If you’re an early-stage AI founder trying to raise a seed round for your GenAI vertical app, know this: You are competing with a startup deploying 100,000 H100s on a single cluster in Tennessee.

This isn’t “software eats the world” anymore. It’s infrastructure eats everything else.

What this means for founders

Founders need to rewire three things:

Efficiency (not growth, per se) may be your #1 KPI. If you burn $20M to hit $10M ARR, you are not scaling. You’re subsidizing. Investors know the difference.

Distribution edge > tech edge. The best products in 2025 aren’t always the most technically impressive. They’re the ones with the fastest GTM loop, the strongest personal brand, or the clearest wedge. The founder-as-channel is no longer a hack. It’s table stakes.

Services are not a detour. The fastest way to build a great product isn’t wireframes. It’s doing the work manually, then turning your insights into code. Services give you signal. They expose friction points that no customer discovery call ever will. They clarify what’s worth automating.

Speed still matters—but only when it compounds. Capital still matters—but only when it’s respected. And ARR still matters—but only when it’s real.

If 2021 was the year of the flex, 2025 is the year of the filter.

Filtered capital, filtered founders, filtered products that actually work.

The game is simpler now:

→ Make something people pay for.

→ Spend less than you make.

→ Build slow, but don’t stop.

The founders who internalize this—who prioritize taste over trends, and precision over praise—will not only survive this cycle, they’ll own the next one.

Newsworthy Stories

FinTech M&A Surge in June. Over 400 fintech M&A deals have closed YTD, with North America claiming 39% and EV multiples averaging ~4.4× revenue. Payments firms led with a 28% YoY volume jump. Deregulation and low barriers are fueling consolidation. It’s a prime window for lean, recurring-revenue fintechs to scale or sell.

U.S. Senate Passes Stablecoin Regulation Bill. The U.S. Senate just advanced a federal framework for stablecoins, a milestone in legitimizing digital currencies. The bill aims to provide clarity and infrastructure for on‑ramps/off‑ramps, making stablecoins a mainstream tool for global payments and treasury management. » More

Klarna Launches $40/Month 5G Mobile Plan in U.S. Klarna, leveraging its 25M+ U.S. users, is launching a $40/month unlimited 5G mobile plan via AT&T’s MVNO network. It's part of a broader strategy to transform from BNPL into a full-service neobank. This reflects a growing trend of fintechs vertically integrating to capture more share of consumer wallet and data. » See why

Founder Tips

📌 Product-market fit is noisy at the bottom and quiet at the top. Early traction often looks like chaos—random wins, inconsistent feedback, strange customers. That’s normal. Don’t mistake turbulence for failure. The real signal comes when things stop breaking under pressure.

📌 Fundraising ≠ validation. Money in the bank is a resource, not a result. Many startups raise on narrative, not traction—only to discover later that they solved a story, not a problem. Stay grounded in use cases, not just investor appetite.

📌 If your GTM plan starts with “go viral,” start over. Viral loops are outcomes, not strategies. Focus on atomic distribution: the one person, channel, or moment that predictably drives conversion. Nail that first. Multiply later.

Markets & Assets At-A-Glance

Asset / Market | Value | Vibe Check |

SOFR Rate | 4.31% | ↔️ Holding steady |

WSJ Prime Rate | 7.50% | ↔️ Unchanged |

S&P 500 | 5,974.44 | ↗️ Modestly up |

Nasdaq | 19,240.22 | ↗️ Slightly elevated |

10‑Year Treasury | 4.38% | ↗️ Yield drifting higher |

Gold (spot per oz) | $3,367.66 | ↗️ Slightly eased, still firm |

Bitcoin (BTC) | $104,555 | ↔️ Trading near recent highs |

Non‑Farm Payrolls | +139,000 | ↘️ Cooling, still in range |

US Unemployment Rate | 4.2% | ↔️ Sitting steady |

Market Movers

Equity

Omnicom to Fully Acquire Clemenger Group. Omnicom is negotiating to purchase the remaining ~13% of Clemenger Group, consolidating its agencies under full ownership. A shareholder vote is set for June 30.

ArisInfra Solutions Launches IPO. ArisInfra, a B2B construction‑materials platform backed by Pharmeasy cofounder, filed for a ₹500 cr (~$60 m) IPO, launching June 18–20, targeting infrastructure growth.

Credit

Green Impact Partners amends credit facility & closes term loan. Green Impact Partners executed an amendment to its corporate credit facility and funded a $2M term loan for working capital

Sterling Infrastructure upsizes & extends credit facility. Sterling Infrastructure amended its 2019 credit agreement, extending maturity to 2028 and expanding the facility to a $300M term loan plus $150M revolver

M&A

Salesforce to Buy Informatica for $8B. Salesforce confirmed purchase of Informatica at $25/share—a deal that accelerates its AI data-management strategy. Expected close in early 2026.

Meta Bets $14.8 B for Minority Stake in Scale AI. Meta is acquiring 49% of Scale AI for $14.8 b, integrating its data-labeling platform into Meta’s AI ambitions and bringing CEO Alexandr Wang onboard.

OpenAI Acquires Hardware Firm io for $6.5 B. OpenAI closed its acquisition of Jony Ive’s AI-device startup io, securing key hardware talent and shaping its consumer-device roadmap.

Recent Cirrus Term Sheets & Transactions

📄 $5M Delayed-Draw Term Loan | SaaS (MarTech)

We facilitated a $5M delayed-draw term loan for a fast-growing SaaS company in the marketing tech space.

Proceeds were used to refinance out of a more rigid ABL structure and support working capital and enterprise onboarding. Deal closed under tight timeline with strong execution on both sides.

📄 $4M Delayed-Draw Term Loan | Recreational Sports Brand

We closed a $4M delayed-draw facility ($3M funded upfront) for a leading operator in the recreational sports space.

Despite previous roadblocks across 50+ lenders, we secured multiple offers and structured the ideal solution. This unlocks better cash flow and positions the company for $100M+ in revenue.

Share the love!

“In 2021, the flex was speed. In 2025, the filter is discipline. Only one builds a company that lasts.”

Altitude is the #1 newsletter for founders, operators, dealmakers, and capital allocators aiming to reach their highest potential. Read alongside 3,200+ founders and professionals every other week. 🏔️

To your growth,

Ryan Ridgway, Founder & Managing Partner

Enjoying Altitude?

Connect with Ryan on LinkedIn for more insights on finance, strategy, and the future of capital.